PureCycle Technologies: The Nikola of Recycling

PureCycle Technologies Fails to Address Short Seller Allegations; More Red Flags Surface

Published on August 16, 2021

Hi everyone,

Thanks for subscribing to Funny Business. About a month ago, I published How America’s Most Inspirational Brand Sold Its Soul to the Devil, an article about Chicken Soup for the Soul Entertainment (CSSE). If you haven’t read that article, you might want to check it out. The stock is down over 40% since then.

I plan on additional CSSE coverage in the future, so go ahead and subscribe if you’d like to be the first to see it.

Today, I wanted to cover PureCycle Technologies in another follow-on report. (This was already covered by a short seller, and yes, I will be publishing completely original research soon, but this one was so egregious that I couldn’t help myself.)

For a little background, Hindenburg Research published its scathing short report on Purecycle, a recent ESG-themed SPAC, on May 6th. Please skim that report before continuing if you haven’t already, or a lot of this won’t make sense.

While the information in the report was alarming, as evidenced by the 50%+ decline in share price around the time of the report, PureCycle executives didn’t refute anything in the article. They barely responded at all. On the contrary, they doubled down.

A few highlights about PureCycle:

PCT has no revenue, but lofty projections. If they were to hit their projections, they would be among the fastest growing and most profitable companies in the world. They would be one of the largest recyclers of plastic globally, multiple times larger than peers that have been doing this for decades.

Keep in mind, this executive team has started at least 6 publicly-traded companies in the past, all of which failed while they made millions.

These same people are making millions from PureCycle even though it has yet to prove its business model or produce a dollar in revenue. The CEO, Mike Otworth, has already cleared around $6 million. He has a $750k salary and could make close to that in bonuses.

I believe that past performance is the best indicator of future performance.

The executive team has a history of failures, shareholder losses, and self-enrichment. When you consider this history along with the blatant red flags in PCTs business plan, the current $1.5B market cap makes this an obvious short for me.

This follow-on piece will cover everything that has happened since the Hindenburg Report, as well as some additional red flags I’ve identified in the business model. I hope you enjoy.

Summary

The PureCycle executives had an opportunity to address the Hindenburg Report in their May 17th earnings call. They chose not to. Instead, they doubled down on their wild projections.

8 days after the Hindenburg Report, PCT insiders quietly changed their own compensation plans to more than triple their pay-outs in the event of separation from the company. CFOMichael Dee was also awarded an additional 184,312 options.

On the May 17th earnings call, CFO Michael Dee reassured investors by referencing a lock-up period, where insiders can’t sell their shares until they hit certain milestones. I believe he used misleading language to give investors a false sense of assurance. I show that PCT insiders will be cleared to sell 100% of their shares before the company generates any revenue, let alone profit.

Michael Dee suggested that those writing “negative articles” should read their Leidos report, which outlines their business plan. I did, and found several major red flags in the PCT supply chain and operational plan.

While the PCT team claims their solvent process has been validated in their FEU facility, the Leidos report indicates the opposite.

PCT Claims to have 20-year agreements for both feedstock and offtake. I see holes in these claims since some of PCTs largest “customers” are not contractually obligated to buy anything and since their feedstock suppliers are not contractually obligated to deliver anything.

PCT stressed again on their earnings call that they are creating a premium product that will justify a premium price point. However, in their license agreement with P&G, they are required to match virgin pricing or risk losing the license to their core technology. Their primary distributor is also entitled to this pricing.

I have found glaring inconsistencies in claims around feedstock purities.

I spoke with several manufacturing/recycling executives who literally laughed out loud when I asked about PCTs claims around feedstock purity, manufacturing uptime, and financial projections.

Part 1: Insiders Increasing Pay-Outs to Themselves

The original severance plan stated that CCO David Brenner and CFO Michael Dee would be paid 6-months salary in the event of separation from the company.

The new plan, setup 8 days after the Hindenburg Report, more than triples their pay-out.

Michael Dee was also awarded an additional 184,312 options, for a total of 614,497 options that would vest immediately if he left the company. (source)

For a team planning one of the most ambitious manufacturing build-outs in history, it seems like odd timing to increase the severance pay-out for top executives. If you consider that members of this executive team have taken 6 companies public, all of which imploded while they pocketed millions, I see this as an indication that they are preparing for another implosion and exit where outside shareholders will be left with the bag.

Alternatively, they could be worried that the ongoing class action lawsuit is going to result in their terminations.

Part 2: The Lock-Up Shouldn’t Reassure Shareholders, It Should Worry Them

During the earnings call, CFO Michael Dee tried to reassure shareholders by referencing the lock-up period, where a large percentage of shares are “locked up” and cannot be sold until the company hits certain milestones. Here is what he said:

“This lock-up demonstrates the commitment of management. Over 60% of the 83.5mil shares that went to PCT shareholders are subject to a lock-up which releases 50% of those shares not until plant 1 in Ironton is commissioned. That’s very important. And Only 20% of the shares are released after 6 months.” - Michael Dee (source)

It is hard to understand what he means here. Is a total of 50% released when the plant is commissioned, with another 50% locked up until certain revenue or profitability targets are hit? Is the 20% included in the 50% or is that additional?

I couldn’t tell for sure from his language, so I checked their SEC filing, which I believe provides the clarity that investors deserve.

Here is the clause, copied directly from their SEC filings:

From and after the six-month anniversary of the Closing Date, each Founder (as defined in the Investor Rights Agreement) may sell up to 20% of such Founder’s ParentCo Common Stock and each PCT Unitholder that is not a Founder may sell up to 33.34% of such PCT Unitholder’s ParentCo Common Stock.

From and after the one-year anniversary of the Closing Date, each Founder may sell up to an additional 30% of such Founder’s ParentCo Common Stock and each PCT Unitholder that is not a Founder may sell up to an additional 33.33% of such PCT Unitholder’s ParentCo Common Stock.

From and after the Phase II Facility becoming operational, as certified by Leidos, an independent engineering firm, each Founder may sell up to an additional 50% of such Founder’s ParentCo Common Stock and each PCT Unitholder that is not a Founder may sell up to an additional 33.33% of such PCT shares of ParentCo Common Stock;

This means that 100% of the shares can be sold before the company generates a dollar in revenue, let alone profit. If I were a shareholder, this wouldn’t reassure me, it would worry me, especially considering the track record of the executive team.

The “closing date” referenced above was March 17, 2021, which means that the first unlock is less than a month away at the time of this writing. For CEO Mike Otworth, this means putting away an additional $10-15 million when the company is still a long way off from showing the marketplace that the technology works at scale, or that it can produce a profit.

Just 6 months after the first unlock, he will be able to sell another 30% (est. $15-20 million), regardless of operational progress.

Bulls may say, “But so many shares will still be locked up. The executive team will have every incentive to stay and make the business work.”

Maybe.

As a wise man once said, “Don’t look at the percentage that is locked up, look at the total amount they are able to take off the table right now.” Let’s look at what Mike can take off the table before the company demontrates commercial viability or sells a single pound of plastic.

SPAC Bonus = $5 million (already in his pocket)

Salary = $750,000 (paid out every two weeks)

Tier 1 Unlock = ~$10-15 million (mid-September)

Tier 2 Unlock = ~$15-20 million (mid-March)

This means that Mike could pocket around ~$41 million before accomplishing anything. I do not understand how shareholders are comfortable with this when Mike and the rest of the Innventure crew (formerly XL Techgroup) have a long history of failed technology companies that return almost nothing to investors.

Typically, these types of milestones align with shareholder value (i.e. hitting certain revenue or profitability targets). In the case of PCT, the insiders have rigged the game to enrich themselves without having to build a successful company.

Keep in mind that the founding team had an incubator (XL Techgroup) that helped to take 6 companies public, all of which failed while they made millions. Even the incubator itself was taken public and ultimately had to sell the majority of its assets to pay back creditors when it defaulted on loans due to the fact that none of its ventures created significant cash-flow.

Part 3: Red Flags in the The Leidos Report

On the May 17th earnings call, 10 days after the Hindenburg Report was published, the only vague reference to criticism were these comments from CFO Michael Dee:

“We have seen some of the negative articles… they have not contacted us, they have not talked to us.Best I can tell, they have not read the Leidos report. But most importantly, they’ve not gone to Ironton … I really don’t have time for those who write negative articles who have not made the effort to talk to us, to read the materials, and to go out and actually see the facility.”

While I am not affiliated with Hindenburg, I did contact PureCycle. I asked if I could attend their in-person “analyst day”. They did not respond to my email.

So I followed Michael Dee’s advice and read the Leidos Report, which was a supposedly “independent” engineering report that backed up PureCycle’s technology and business model.

The Leidos Report didn’t assure me, it only raised more red flags.

For example, PureCycle claims that their small-scale pilot plant (the “FEU”) has already proven that the technology works.

This was reiterated by CMO Dustin Olson on the Q1 earnings call.

“The FEU is just a fundamental piece of our machine, and quite frankly, it proves the technology works.” -Dustin Olson

In reality, the Leidos report shows that the FEU has only produced 1,742lbs of polypropylene since it opened last year, with an average yield of 55%. The yield was as low as 32% for materials like carpets, which PCT has claimed will be an important feedstock source.

Let’s be clear. If PureCycle sees yields of 55% in their commercial facility (if it is ever completed), they will burn money with every production run. This doesn’t prove their technology, it does the opposite.

Why? The company’s financial projections are based on yields above ~90%, not 55%. At 55%, all of their COGS skyrocket (raw materials, labor, etc…)

Here are PCTs assumptions, as outlined in the Leidos report.

90% uptime in manufacturing, totaling 7,884 hours per year (wildly unrealistic based on my conversations with manufacturing executives)

Process feedstock at 15,144 lbs per hour.

Achieve a ~90% yield on feedstock that is at least 93.3% pure.

If you multiply these factors, you get to a familiar number:

(7,884 hours per year) x (15,144 lbs per hour) x (90% yield) = ~107 million pounds per year

Dustin Olson reiterated this number in the Q1 earnings call.

“But the key point is our first facility- commercial size facility- which is 107 million per year in Ironton, is on track, okay?”

There are a few holes in this math.

First, 90% uptime is highly unlikely for any manufacturing company, much less a recycling company, and much less a startup.

Here’s what one manufacturing executive told me about uptime with this type of equipment.

“While 90% is technically feasible, it is completely unrealistic and unprecedented. 85% is considered amazing, world class. Most are far below that.”

As an aside, this same executive laughed out loud when I showed him PureCycle’s financial projections, saying “This looks like something I put together in college.”

A different executive, with deep experience in polypropylene recycling, had this to say.

“I would be very skeptical about a 90% uptime… we do run 24/7, but only for 5 days a week. The other two we’re down…”

He continued…

“This equipment never works as advertised. If a line is advertised at 8,000 pph, it will actually do 6,000 pph. They are also going to have to bolt on an entire mechanical process at the front end. It’s a dirty process, and things need to be cleaned. We have 10-15 extra guys each shift just clearing debris.”

*As an aside - PCT has budgeted for just 1-2 “waste technicians” per shift, per the Leidos Report. I believe they are massively underestimating the staffing requirements for their facilities, which is also evidenced by the number of forklift drivers they are budgeting for.*

When asked about yield, the same executive said 90% yields are highly unlikely because you would have to start with feedstock that is higher than 90% pure, which he says he has never seen before. Additionally, he noted in-process losses.

“High purity feedstock like they are claiming to have, 85% and higher, it just doesn’t exist. You lose 25% of your feedstock right off the bat from contamination, and that’s on a good day… you can lose about another 10% in-process. You never know what suppliers are going to send you.”

To be sure, I interviewed another recycling executive with 20 years of experience. I asked about polypropylene feedstock.

“I do not know of any post-consumer polypropylene with purities that high… I don’t know of any huge volumes of PP just waiting to be purchased in general. The market is really tight right now for material.”

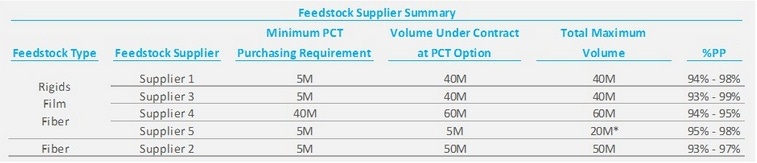

So, PCT has found multiple sources of vast quantities of ultra-pure polypropylene feedstock (that experts say doesn’t exist). They have negotiated guaranteed supply agreements with these suppliers.

There’s just one problem. The Leidos Report notes that these feedstock “contracts” aren’t actually binding.

“There are no penalties stated in the agreements for failure of either party to deliver and/or accept the committed quantity of feedstock.” (Page 61 of the Leidos Report)

So, the feedstock suppliers don’t actually have to deliver anything.

This may explain why PCT is so eager to disclose its customers and vendors, but redacted the name of all of its suppliers from the Leidos Engineering report. And then there’s this tidbit.

The Leidos team also states that it has not validated the legitimacy or enforceability of the feedstock agreements.

In the original pitch deck, they claim the lowest purity feedstock they have under contract is 93% polypropylene.

However, in the Leidos report, purities are as low as 79% for some suppliers and 85% for what appears to be the largest supplier.

Let’s take a look at the Leidos summary:

Based on our review, and provided that the amount of PET and other high melting point plastics in the feedstock in the feedstock is minimized, we are of the opinion that the Phase II Facility should be capable of achieving the KMPS guarantees, and if designed, constructed, operated, and maintained as currently proposed by the Company, including resolution of outstanding design issues, the Phase II Facility should be capable of an annual UPRP production level of approximately 107,616,919 lb during mature operations, based on a minimum polypropylene content of at least 93.3 percent in the feedstock and maximum polypropylene process loss of 3.3 percent of the feedstock for a combined recovery of 90.0 percent of the feedstock.

Putting aside that the extraction process is completely unproven at scale and that the company is probably under-estimating COGS and in-process losses, let’s continue to think about feedstock. What do we really know about PCT’s feedstock strategy?

Leidos says that PCT could theoretically produce recycled PP if a few conditions are met, one of which is the company securing high-purity feedstock (93%+).

Experts have said this type of feedstock doesn’t exist. Names of all suppliers have been redacted from all public filings.

Leidos didn’t validate the enforceability of the feedstock agreements, but did say that there are no stated penalties for failure to deliver.

“The ability to source feedstock with high polypropylene content” is listed as a risk factor in PCT’s SEC filings.

Other recycling startups have failed due to the inability to get the right type of feedstock.

There are discrepancies between what PCT told investors and what the Leidos report uncovered.

Another red flag in the Leidos report is sales commitments.

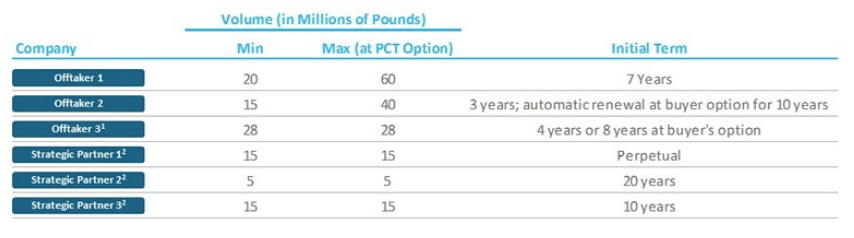

CEO Mike Otworth has repeatedly claimed that the business has pre-sold 20 years’ output from the first plant. Companies like Nikola and Lordstown made similar claims.

“PureCycle has signed contracts with P&G, Milliken, Nestlé and L’Oréal to produce rPP and has presold more than 20 years of output from our Ohio plant.” -CEO Mike Otworth (source)

This can be seen in their original pitch deck as well.

In reality, many of these partnerships are hollow.

Offtaker 1, for example, is not an actual buyer. While they don’t name this person and/or company, they do show that it is an outside sales representative, not an actual customer.

Other purported partnerships appear to be non-binding:

It is unclear who PCT’s customers are, and if the sales agreements are binding. Leidos, the supposed independent engineer, disclosed that it did not validate the enforceability of the sales agreements.

Part 4: Doubling Down

After the Hindenburg Report, PCT could have toned down their aggressive projections. Instead, they doubled down.

Anyone who has worked in manufacturing will tell you that a new factory build-out is a difficult process.

If you haven’t worked in manufacturing, imagine implementing a new ERP. That’s a headache for any company. Now, add physically rebuilding your entire office in another part of the country, and hiring a completely new team to run that office.

For a startup, it’s especially grueling.

But what about a startup building ~7 multi-hundred-million-dollar factories at the same time? While that seems impossible, that’s exactly what PureCycle pitched in their original fundraising deck.

While the Q1 earnings call would have been a good time to soften this aggressive ramp-up schedule, instead, they doubled down.

Per the recent Q2 earnings call, they are now planning to build ten factories, and they also announced a possible 11th plant in South Korea, all in ~3.5 years. Here’s the updated ramp-up schedule (which doesn’t include the South Korea plant).

While I try to avoid hyperbole and stick to the facts, this is just completely ridiculous. I worked for a manufacturing startup for years and it took nearly a decade to build two plants, and people were stretched thin to make that happen.

Even if you have a bullish view on PCT and are confident in the executive team. Even if you ignore all of the red flags (past and present)... this plan is ludicrous.

Even if this build-out were possible, how could anyone think it’s the right move to build this many factories before proving out the technology and business model at the first factory? Don’t shareholders want to see profitable on-spec production at the first plant before pouring billions into additional plants?

Perhaps this is why no independent analyst has issued a “buy rating” for PCT.

The only analysts that have posted positive “buy ratings” are all affiliated with the firms that helped PCT raise money. I see this as a serious conflict of interest. Some of these firms, such as Roth Capital, are so famous for bringing fraudelent companies to public markets that they have even been covered in documentaries about fraud.

The only independent author on Seeking Alpha shares my skepticism.

The stock price of PCT may go up and down, but my money is long on it going to zero.

Conclusion

PureCycle is run by a team with a long track record of destroying shareholder value.

The same team claims that P&G invented a world-changing technology, that can magically remove all contaminants from one of the most difficult materials to recycle.

This is something the worlds top chemical companies have been trying to figure out for decades.

They claim P&G simply licensed this technology to an unknown startup for a nominal fee.

They claim they will ramp-up this unproven technology at an unprecedented pace, making them one of the largest recyclers of plastic in the world in just a few years.

They claim they will produce massive profits almost immediately, putting them in league with the world’s most profitable tech companies.

Based on my research, I don’t see any of this happening.

I predict the following over the next few years -

PureCycle will see additional delays in factory build-outs. They will blame this on supply chain issues out of their control, likely their vendors.

If they get one plant up and running, which is unlikely, it will have major issues and will fail to be profitable. They will see challenges related to feedstock purity, supply, and pricing.

They will continue to issue shares and raise money for as long as they can so that they can maintain their high salaries, stock-based compensation, and bonuses. Keep the party going!

Eventually, when it is impossible to raise enough capital to keep the charade going, insiders will start selling, executive and employee turnover will rise, and the company will eventually get delisted and file for bankruptcy.

I am short $PCT.

If you enjoyed this article, please consider subscribing. Each new subscriber means a lot. You encourage me to keep researching and writing. Plus, you’ll be the first to see additional coverage on companies like PureCycle Technologies and Chicken Soup for the Soul Entertainment, as well as brand new reports on companies that no one else has published on in the past.

DISCLAIMER:

I sometimes write about publicly-traded companies. I am not a financial advisor and I hold no financial registrations. You should never use my research as due-diligence or investment advice. My research is for entertainment only. I am not responsible for investment losses. I do actively invest, and you should assume I may have long/short positions in the companies I write about. I am not responsible for your losses.